Written By Most

How to claim pension tax relief often worth thousands of pounds

This is one of the greatest unlocks in UK personal finance and most people don’t know about it.

If you’re a higher or additional rate taxpayer, this probably affects you because of a quirk in the way HMRC handles pension tax relief.

Millions of people in the UK short-changed every year

PensionBee revealed that between 2016 and 2021, £1.3 billion in pension tax relief went unclaimed. Here’s how:

If you’re a higher or additional rate taxpayer, you should get extra relief to match your tax rate (40% or 45%).

The problem is many people don’t get this extra relief automatically so are missing out on an extra 20% - 25%.

If you don’t contact HMRC to claim it, the taxman keeps your money (course he does).

Btw, we've done a few episodes recently about pensions including this banger from Tom McPhail (video below) explaining how to sort your pension this year.

A simple explanation of pension tax relief

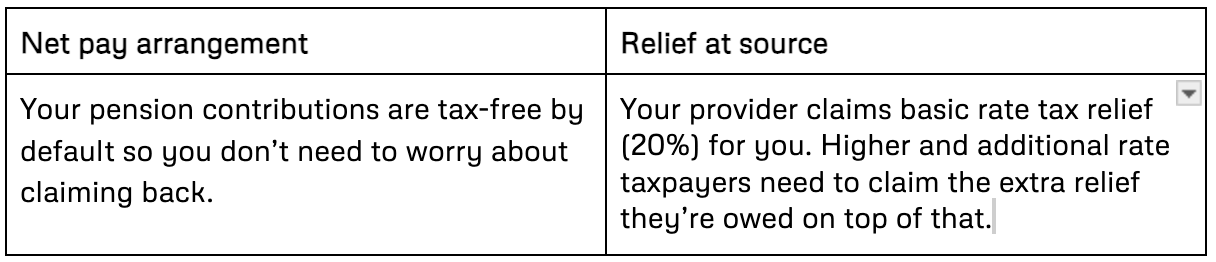

The money you contribute to your pension is supposed to go in tax-free. There are two ways most employees contribute to their workplace pensions: through a net-pay arrangement or a relief at source scheme.

Net-pay arrangement

Your contributions are made before you pay any tax, so you’re not owed anything because you haven’t been taxed on your contributions.

Relief at source

Your contributions are made after you’ve paid income tax. This means the government is supposed to return what you’ve paid in tax on your pension contributions, otherwise they’re not tax free.

You get taxed 20% on that £1 as a basic rate tax payer, before you’ve made your contributions, so you actually only put in 80p.

The government owes you 20p, to top it back up to £1.

Although basic rate tax is 20%, basic rate tax relief is actually 25% because of, well, maths.

If you got 20% relief on an 80p contribution, you’d only get 16p back whereas 25% on 80p gets you 20p - and back to the full pre-tax £1.

By the way, the £1 is the ‘gross contribution’ - not the 80p - i.e. gross contributions include basic rate relief, which is important for understanding Sarah’s example below.

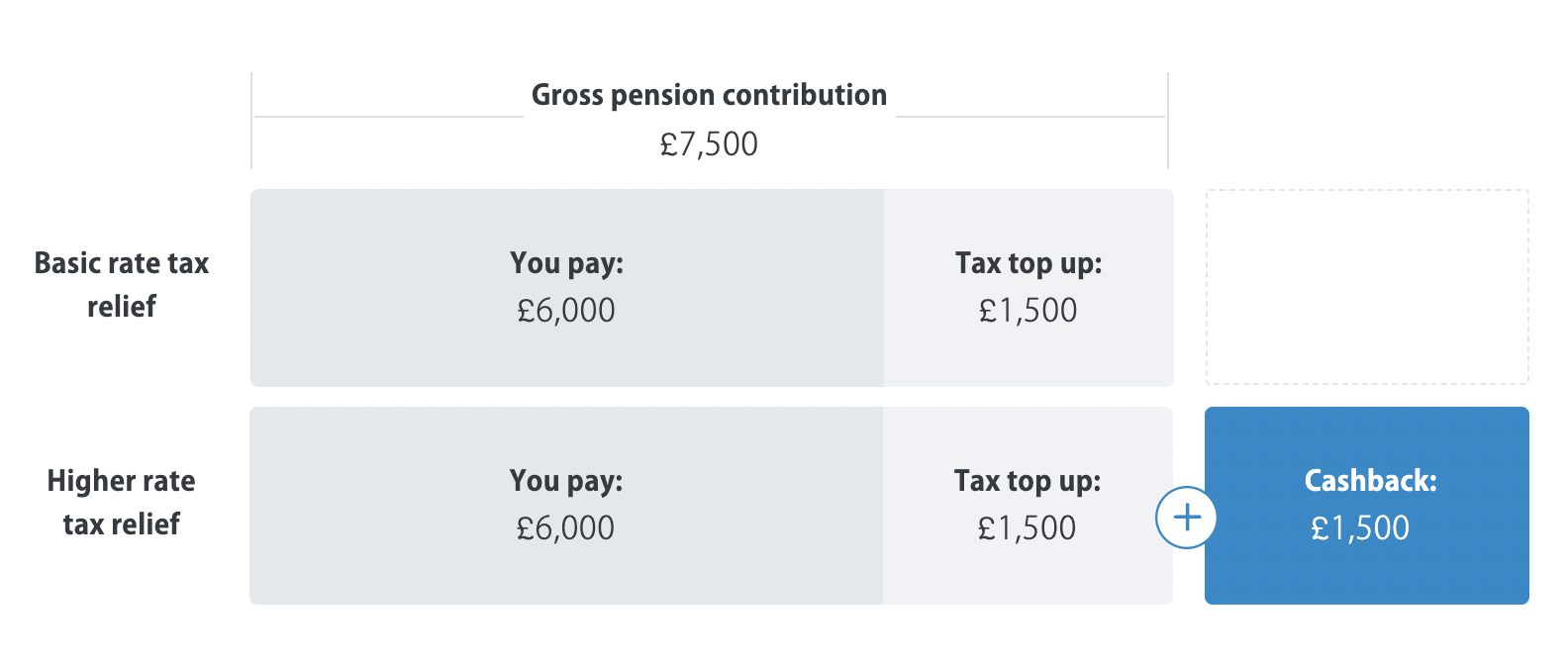

Imagine the case of Sarah

She earns £60,000 a year so is a higher rate taxpayer (paying 40%).

She wants to make a gross contribution of £7,500.

She puts £6,000 into her self-invested personal pension (SIPP).

Her provider automatically adds her 25% tax relief at source (£1,500 on £6,000), making her gross contribution £7,500 which is what she’d wanted.

But Sarah’s a higher rate taxpayer, so she’s entitled to 40% tax relief on the gross contribution of £7,500 and only received 20% so far (£1,500).

This means she’s owed another £1,500, but she won’t get it unless she submits a claim.

And that’s from just one year - she can go back four tax years - so if she’s eligible, she could claim £6,000. It’s pretty mind-blowing.

You can see what you might be owed, if you know what you’ve contributed, using this calculator.

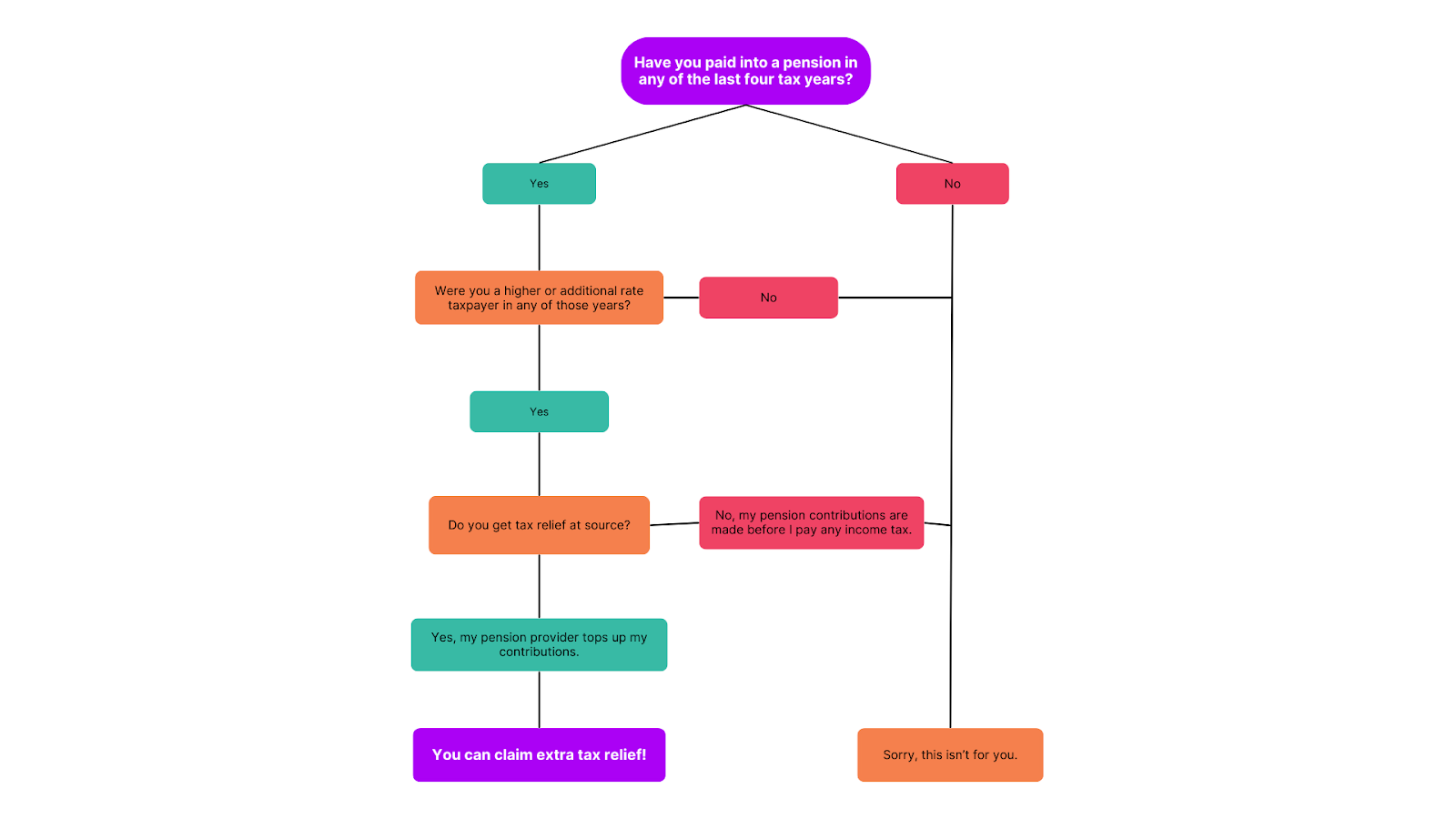

How to work out if you’re eligible to claim pension tax relief

If you earn over £50,270 and contribute to a relief at source pension (this year or in the last 4 years), you’re almost certainly missing out on some money. This is true for both workplace pensions and SIPPs.

Still not sure? Use this flowchart to work out if you’re owed some of the missing millions.

How to claim pension tax relief

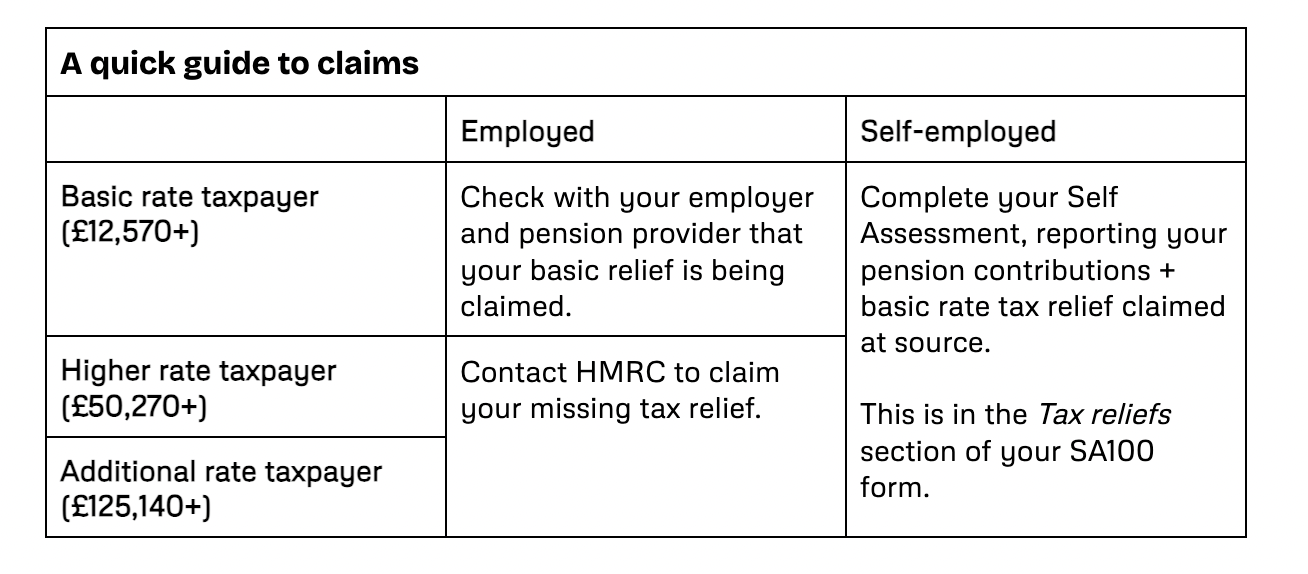

If you’re a basic rate taxpayer

If you’re paying 20% in income tax and making pension contributions, you should be sorted already unless a mistake has been made (in which case contact HMRC, as explained below).

If you’re a higher or additional rate taxpayer

If you’ve paid 40% or 45% tax on some of your earnings and contributed to a relief at source pension, you should be eligible for extra tax relief.

Employed - and a higher rate or additional rate taxpayer

You’ll need to contact HMRC by post, phone, or online form. They have a clear process to follow, so it hopefully won’t take too long.

You can complete a Self Assessment form instead, but this can be more complicated and time-consuming.

Self-employed - and a higher rate or additional rate taxpayer

You can contact HMRC by post, phone, or online form for anything your owed for contributions you’ve already made.

Going forward, in your annual Self Assessment, report your gross pension contributions (i.e. what you paid, as well as the tax relief you’ve already received) in the Tax reliefs section.

HMRC will use this to calculate any additional tax relief you’re owed.

What you need to make a pension tax relief claim

HMRC needs certain information to process pension tax relief claims. Before contacting them, you’ll need to have:

The type of pension (e.g. workplace, SIPP, etc.)

The company providing your pension

Your pension contributions in each tax year you’re claiming for

Proof of your contributions made in each tax year you’re claiming for

Your payroll number or pension reference number

How pension tax relief gets paid to you

Unlike your basic rate relief, the extra relief you claim doesn’t go directly into your pension.

You can choose to receive it as:

A change to your tax code (reducing how much you’ll owe next tax year)

A reduction in your tax bill (reducing how much you owe in the current year)

Of course, the sensible choice is to put the money into your pension - that’s the point of it - but the choice is yours.

How to get the most out of your pension so you can retire well

This is just one small part of getting the most from your pension so you can have a good retirement. We’ve written a free guide on pensions so you can see how this extra pension tax relief can fit into an effective retirement strategy.

If you want to get the most from pension tax relief, you should:

Claim for the last four tax years, if eligible. (Sarah, from our earlier example, would get £6,000 back).

You can also work with one of our financial advisors for retirement planning.

Key steps to sort your pension tax relief

- Check your tax records from the last four years, noting which years you were a higher or additional rate taxpayer.

- Find out whether you got tax relief at source and how much you contributed to your pension in those tax years.

- Pull together all the information HMRC needs.

- Contact HMRC and make your claim.

Now, go and get what you’re owed - and let us know if you do 🚀

PS if you have a pension with Nest then check out this episode about how they invest your money.

And if you want even more juice on how to get the most out of your pension, then check this episode with Tom McPhail on the pensions crisis.

—

This is not financial advice. The reason it’s not financial advice is because it’s not tailored to you. We are here to talk about the principles of building wealth but if you want personalised help, it’s worth speaking to a financial advisor. As with everything financial, please do your own research. We really encourage that because no one cares more about your money than you and if you learn the basics then it’s life-changing.